AML/CTF Is No Longer Just a Compliance Task

For many years, AML/CTF compliance has been treated as a necessary administrative obligation – a set of documents completed during onboarding, filed away, and rarely revisited unless requested.

That approach is no longer sufficient.

Across Australia, Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) compliance is entering a new phase. Regulatory expectations are increasing, enforcement is becoming more proactive, and professional firms are now expected to demonstrate not just compliance, but control, consistency, and accountability.

At the centre of these changes is AUSTRAC, which modernises Australia’s AML/CTF framework to ensure it remains effective in a digital, fast-moving economy.

For accounting and professional services firms, the message is clear:

AML/CTF compliance is becoming an operational system – not a one-off task.

Firms across the industry are reevaluating their management of client verification, risk assessment, and record-keeping. The focus is no longer on adding complexity but on ensuring AML/CTF obligations are met consistently and defensibly through structured client verification workflows rather than fragmented manual processes.

What Is AML/CTF compliance— in Practical Terms?

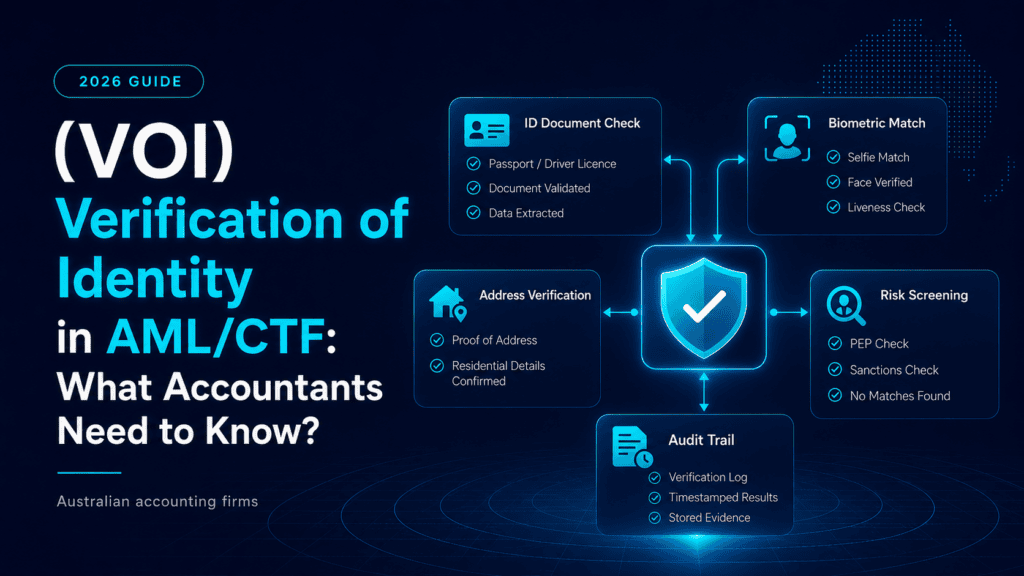

AML/CTF compliance refers to the legal and operational framework designed to prevent criminals from using legitimate businesses to launder money or finance terrorism.

In practical terms, it requires firms to:

- Verify the identity of clients

- Understand who they are dealing with and why

- Assess and manage financial crime risks

- Keep accurate and retrievable records

- Monitor client relationships over time

- Demonstrate compliance if reviewed or audited

For accounting and advisory firms, these obligations are not theoretical. Professionals often act as the gateway to financial systems – onboarding clients, managing structures, handling sensitive data, and interacting with regulatory bodies.

As a result, accounting firms play a critical role in protecting the integrity of Australia’s financial system.

Why Australia Is Reforming the AML/CTF Framework

Australia’s AML/CTF regime has been in place for many years, but the environment it was designed for has changed significantly.

Key drivers behind the reforms include:

- Digital client onboarding becoming the norm

- Increasingly complex ownership and control structures

- Growth in cyber-enabled financial crime

- Fragmented and inconsistent compliance processes

- Over-reliance on static documentation rather than real risk assessment

The existing framework has often been criticised for being overly complex, document-heavy, and difficult to apply consistently – particularly for small and mid-sized firms.

AUSTRAC’s reform agenda is designed to modernise the system by:

- Simplifying requirements

- Strengthening risk-based decision-making

- Improving consistency across industries

- Making compliance outcomes more effective in practice

The objective is not to increase red tape, but to ensure AML/CTF controls genuinely reduce financial crime risk.

Key AML/CTF Program Reforms Firms Must Understand

The reforms place renewed emphasis on how AML/CTF programs operate, not just whether they exist.

1. Simpler, More Flexible AML/CTF Programs

The traditional “Part A / Part B” structure is being replaced with a more streamlined approach.

Firms are expected to:

- Design programs based on their actual risk profile

- Avoid generic, templated documentation

- Clearly document how risks are identified and managed

This flexibility allows firms to tailor compliance – but also increases accountability.

2. Stronger and More Current Risk Assessments

Risk assessment is becoming the foundation of AML/CTF compliance.

Firms must understand:

- The nature of their clients

- The services they provide

- Where higher-risk scenarios exist

- How risks are mitigated and reviewed

Outdated or static assessments will no longer meet regulatory expectations.

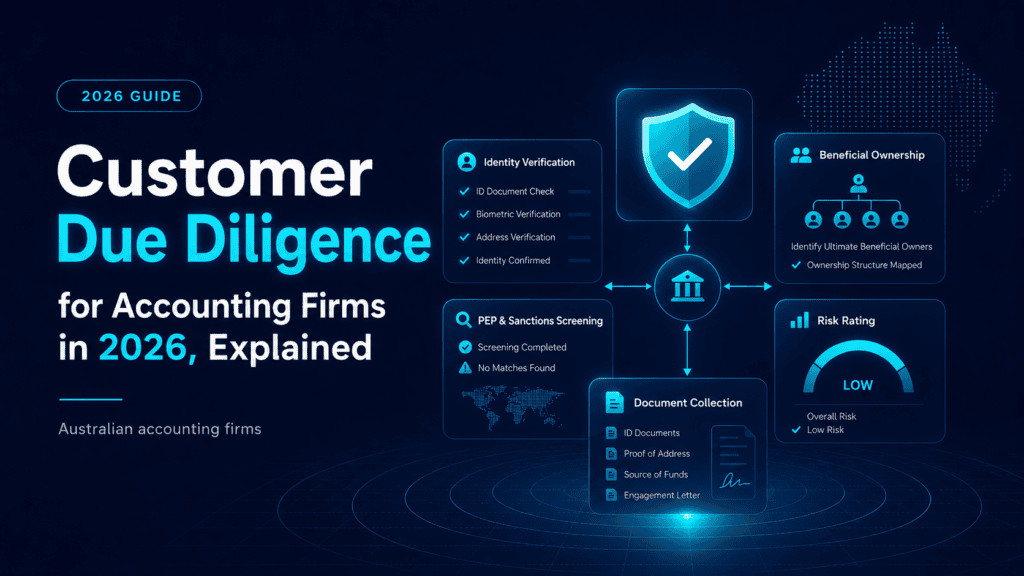

3. Ongoing Customer Due Diligence

AML/CTF obligations no longer end at onboarding.

Firms are expected to:

- Monitor client relationships over time

- Update client information when circumstances change

- Identify shifts in ownership, behaviour, or risk

- Maintain clear records of verification activity

This reinforces the shift from one-time checks to continuous oversight.

4. Record-Keeping and Audit Readiness

Record-keeping is no longer about storing documents – it is about retrievability and traceability.

Firms must be able to:

- Produce evidence quickly when requested

- Show how compliance decisions were made

- Demonstrate consistency across client files

- Maintain clear audit trails

Scattered or manual records significantly increase compliance risk.

5. Clear Accountability and Governance

AML/CTF responsibility must be clearly assigned.

Firms need:

- Defined roles and accountability

- Management oversight of compliance frameworks

- Escalation processes for higher-risk matters

- Ongoing staff awareness and training

Compliance is now a firm-wide responsibility, not an isolated task.

What These Reforms Mean for Accounting and Advisory Firms

For accounting and professional services firms, AML/CTF reform has direct operational implications.

Firms will need to:

- Spend more time verifying and reviewing client information

- Apply compliance standards consistently across teams

- Handle higher onboarding volumes without sacrificing accuracy

- Respond confidently to regulatory enquiries

- Reduce dependency on individual staff knowledge

Importantly, AML/CTF compliance is no longer just a regulatory issue – it is a reputational one. Clients increasingly expect their advisers to operate with strong governance, transparency, and control.

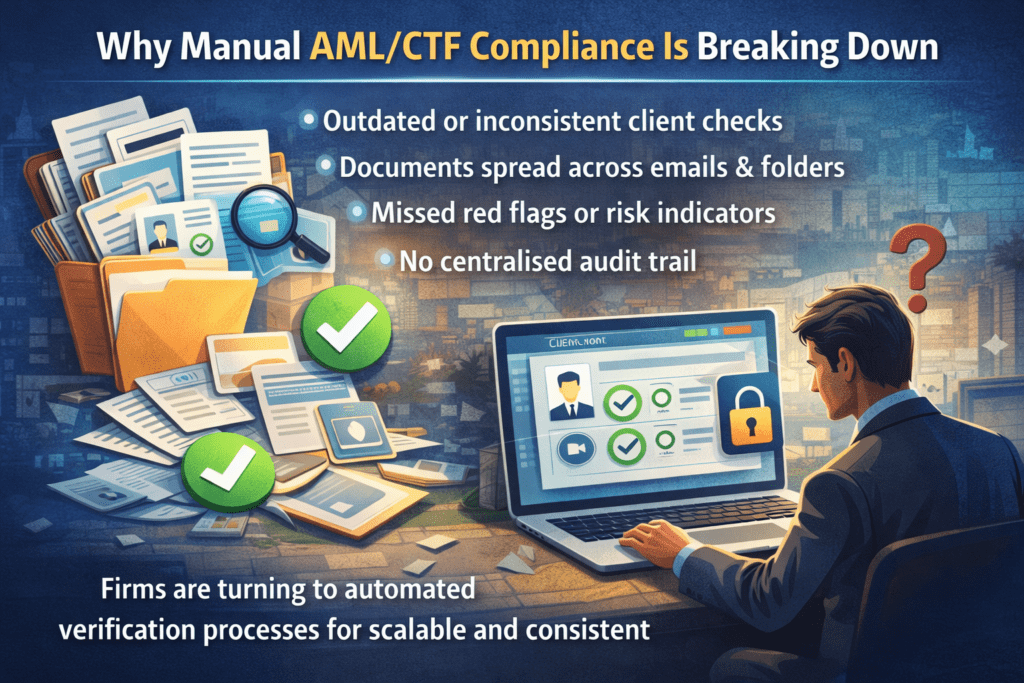

Why Manual AML/CTF Compliance Is No Longer Sustainable

Many firms still rely on:

- Emails and PDFs

- Manual checklists

- Spreadsheets

- Disconnected file storage

- Individual staff experience

While workable at low volume, these approaches struggle as compliance requirements increase.

Common failure points include:

- Missed or outdated verification

- Inconsistent application of rules

- Limited audit trails

- Staff dependency and turnover risk

- Time pressure during peak periods

Increasingly, compliance issues arise not from intent, but from process limitations. Client identity checks, supporting documents, and verification evidence are often spread across systems, making it difficult to demonstrate compliance with confidence.

As a result, many firms are moving toward automated client verification frameworks that standardise how AML/CTF checks are performed, recorded, and retained – reducing reliance on manual intervention and improving audit readiness.

How Leading Firms Are Responding to AML/CTF Reform

Rather than expanding administrative teams or adding more manual checks, many firms are re-engineering how compliance fits into their operations.

Common approaches include:

- Automating client identity and verification steps

- Centralising AML/CTF records and evidence

- Embedding risk assessment into onboarding workflows

- Ensuring compliance actions are logged and traceable

These changes are driven by the need for consistency, accuracy, and confidence – particularly as regulatory scrutiny increases.

Firms adopting structured verification systems early are finding it easier to adapt to reform while maintaining service quality and operational efficiency.

The Future of AML/CTF Compliance: Systems Over Spreadsheets

The direction of AML/CTF compliance is clear.

Future-ready firms will:

- Treat compliance as an integrated system

- Centralise verification and evidence

- Standardise risk-based decisions

- Maintain real-time visibility over compliance status

- Reduce reliance on manual workarounds

Automation does not remove responsibility – it supports consistency, scalability, and defensibility as expectations continue to rise.

Preparing With Confidence

AML/CTF compliance in Australia is evolving rapidly.

The focus is shifting from forms to frameworks, from documents to decisions, and from reactive compliance to proactive control.

Firms that treat compliance as a system – supported by clear processes and reliable client verification solutions – will be better positioned to meet regulatory expectations without disruption.

Preparing early allows firms to move forward with confidence rather than responding under pressure.