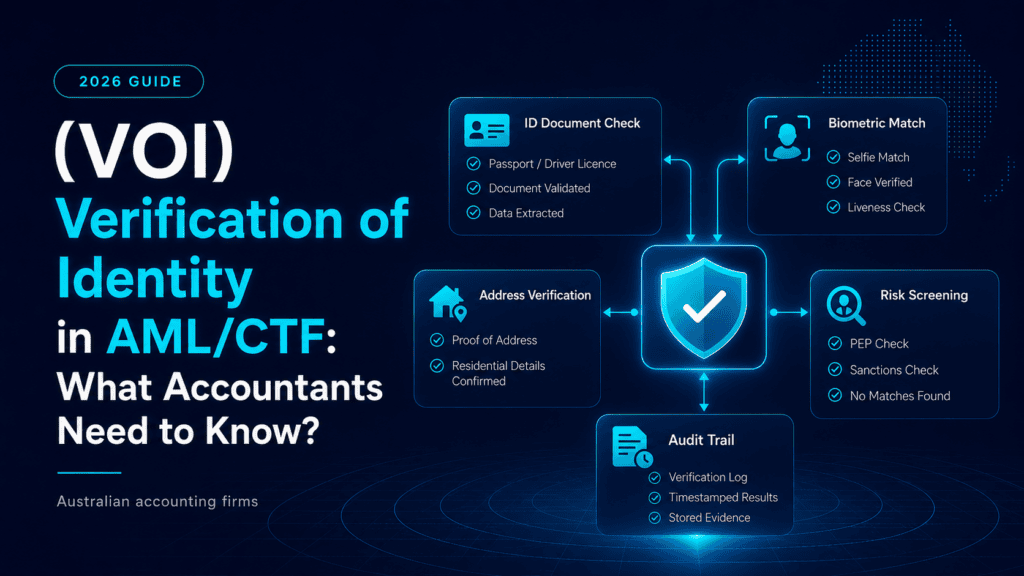

This is the question every accountant in Australia is asking right now and it is more nuanced than a simple yes or no.

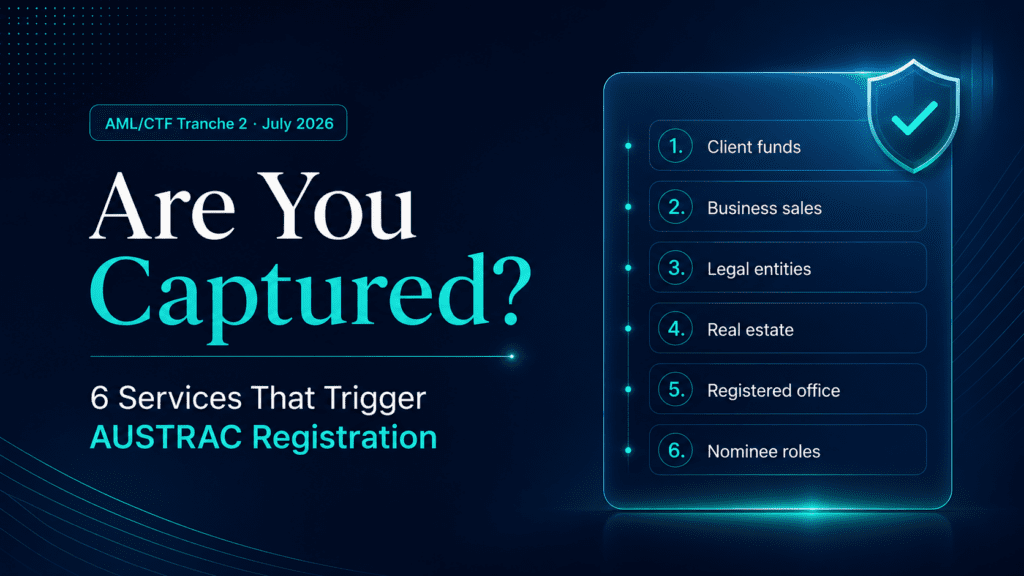

From July 1, 2026, certain accounting services trigger mandatory registration with AUSTRAC under Australia’s AML/CTF Tranche 2 reforms. But not every accounting firm is captured. Whether you need to register depends entirely on which services you actually provide not how large your firm is, how long you have been operating, or what your primary title is.This guide gives you a breakdown of the six categories of designated services that capture accountants, with real-world examples for each. By the end, you will know exactly whether your firm needs to register and what to do next.

The single most important rule:

If you provide even ONE designated service to even ONE client, your entire firm becomes a reporting entity regardless of size, structure, or how rarely you provide that service.

Start Here: The 6-Question Self-Assessment

This is the question every accountant in Australia is asking right now and it is more nuanced than a simple yes or no.

| If you answer YES to any of these questions… | Yes / No |

|---|---|

| Do you manage client funds, accounts, or assets on their behalf? | ☐ Yes ☐ No |

| Do you help clients buy, sell, or transfer a business? | ☐ Yes ☐ No |

| Do you set up, operate, or manage a company, trust, or SMSF for clients? | ☐ Yes ☐ No |

| Do you provide a registered office address for any client? | ☐ Yes ☐ No |

| Do you act as a nominee director, secretary, or trustee for any client? | ☐ Yes ☐ No |

| Do you assist clients with buying or selling real property? | ☐ Yes ☐ No |

If you answered YES to any question above: Your firm is likely a reporting entity. You must enrol with AUSTRAC, develop an AML/CTF program, and have client verification in place before July 1, 2026. Read on to understand exactly what this means for your practice.

Already know your firm is captured?

Skip straight to seeing how VERA handles client verification — the most operationally demanding part of AML/CTF compliance. Book a free 20-minute demo and we will show you exactly how it works in your practice.

👉 Book Your Free VERA Demo6 designated service categories that capture accountants

AUSTRAC defines six categories of designated services that bring accounting firms under the AML/CTF regime. Below is explanation of each, with real-world examples of how they apply in practice.

WHAT This covers any situation where you hold, manage, or have authority over client funds or financial assets on their behalf beyond simply receiving payment for your professional fees.

EG Real-world examples:

- Holding client funds in a trust account pending settlement of a transaction

- Operating a bank account on behalf of a client entity

- Managing investments or portfolio assets for a client

- Acting as trustee of a client’s discretionary or unit trust and making payment decisions

- Receiving and distributing rental income on behalf of a client

Who this captures: Any accountant who manages client money — including holding funds in trust, operating accounts, or managing assets — is captured. This is one of the most common triggers for accounting firms.

WHAT This captures your involvement in business transactions — specifically where you assist with or facilitate the acquisition, sale, or transfer of ownership of a legal entity or its assets.

EG Real-world examples:

- Advising on or structuring the sale of a client’s business

- Preparing or reviewing business sale agreements

- Acting as an intermediary in a business acquisition

- Facilitating the transfer of shares in a company as part of a business sale

- Assisting with the transfer of business assets — goodwill, equipment, IP — between entities

Who this captures: Accountants who advise on or facilitate business sales and acquisitions — a core service for many business advisory practices — are captured under this category.

WHAT This is one of the broadest categories — and one that catches many accountants by surprise. If you help establish, administer, or manage any legal structure for a client, you are likely providing a designated service.

EG Real-world examples:

- Setting up a company for a client through ASIC

- Establishing a discretionary trust or unit trust for a client

- Setting up a Self-Managed Superannuation Fund (SMSF) for a client

- Acting as the registered agent for a corporate trustee

- Managing the ongoing compliance of a company — annual returns, ASIC updates

- Establishing a partnership structure for clients

Who this captures: This is the category that captures the widest range of accounting practices. If you do any company formations, trust setups, or SMSF establishments — even occasionally — you are a reporting entity.

WHAT Accountants who assist clients with property transactions — beyond simply providing tax advice on the transaction — may be captured under this category.

EG Real-world examples:

- Assisting a client to structure a property acquisition through a trust or SMSF

- Facilitating the transfer of real property between related entities

- Managing conveyancing processes on behalf of a client entity you operate

- Assisting with the purchase of commercial property as part of a business acquisition

Who this captures: This category is most relevant to accountants who are actively involved in structuring or facilitating property transactions — not those who simply provide tax advice after the fact. However, the line is not always clear, and legal advice is recommended if you are uncertain.

WHAT This is the most commonly overlooked trigger and it catches many accountants completely off guard. If your firm’s address appears as the registered office for any client entity with ASIC, you are providing a designated service.

EG Real-world examples:

- Your firm’s address is listed as the registered office for a client company

- You receive ASIC correspondence on behalf of a client entity

- You provide a “care of” address for a client trust or SMSF

- You have historically provided a registered office as a standard part of your company secretarial services

Who this captures: This is arguably the most widespread trigger for small and mid-sized accounting practices. If you currently provide this service to even one client and most practices do, you are a reporting entity from July 1, 2026.

WHAT If you or any person in your firm acts as a nominated director, company secretary, or trustee on behalf of a client, this is a designated service. This applies even if the role is largely administrative.

EG Real-world examples:

- A partner or staff member serving as a director of a client company

- Serving as company secretary for a client entity

- Acting as trustee or corporate trustee of a client’s trust

- Providing a nominee director service to non-resident clients establishing Australian entities

Who this captures: Accountants who provide nominee or officeholder services, even where this is a minor part of their practice are captured. This is particularly relevant for firms serving international clients or providing company secretarial services.

Common Scenarios: Are You Captured?

Here is how the rules apply to the most common accounting practice types in Australia:

Tax return preparation only (no advisory, no entities) → NOT CAPTURED

If your practice focuses purely on preparing individual or business tax returns and providing tax advice — without managing client money, setting up entities, or providing registered office addresses — you are not providing any designated services and do not need to register.

Bookkeeping firm that manages client bank accounts or payroll accounts → YES CAPTURED

Managing client money — including operating accounts on a client’s behalf — is a designated service. Bookkeeping firms that have authority over client accounts are captured.

Accounting firm with some clients who also receive business sale advice → YES CAPTURED

Assisting with business acquisitions and sales is a designated service. Even if this is a minor part of your practice, it triggers reporting entity status for your entire firm.

Large national firm offering a full range of services → YES CAPTURED

National firms providing any combination of entity management, business advisory, trust administration, or registered office services are clearly captured. The compliance burden is significant, and automation is essential at scale.

Business advisory practice (including entity setups, SMSFs, trust administration) → YES CAPTURED

If you establish companies, trusts, or SMSFs for clients, or help manage those structures, you are providing designated services. This is one of the most common triggers for full-service accounting practices in Australia.

Sole practitioner providing tax and bookkeeping only → NOT CAPTURED

If you prepare tax returns and financial statements and do not manage client money, set up entities, or provide a registered office address, you are not captured — regardless of how many clients you have.

Firm that provides registered office addresses for client companies → YES CAPTURED

Providing a registered office address is a designated service. If your firm’s address appears on ASIC records for any client entity, you are a reporting entity from July 1, 2026 — even if this is the only designated service you provide.

What If I Am Still Not Sure?

AUSTRAC has published an online tool specifically to help accountants determine their obligations. The ‘Check If You Are Regulated’ questionnaire walks you through a series of questions about the services you provide and tells you whether you are likely captured.

You can access it at: Click Here to Redirect

Important caveat:

AUSTRAC’s online tool provides guidance not a formal determination. If your services fall into a grey area, or if you provide complex structures involving multiple types of designated services, you should seek legal advice from a compliance specialist familiar with the AML/CTF Act before July 1, 2026.

What Do You Do If Your Firm Is Captured?

If one or more of the designated services above applies to your practice, here is your immediate action list:

Step 5 is where most practices get stuck. VERA makes it simple.

Client verification is the most operationally intensive part of AML/CTF compliance. VERA automates Face-ID checks, document verification, AML/CTF screening, risk scoring, engagement letter generation, and record keeping — reducing 45 minutes of manual work to approximately 3 minutes per client. Deploys in 2 weeks. No lock-in.

👉 Book Your Free VERA DemoP.S. One of the most common mistakes practices make is assuming that because they primarily do tax returns, they are not captured. If you provide even a single registered office address for even one client, you are a reporting entity under Tranche 2. The time to check is now, not in June.

About Nex Automate

Nex Automate is an Australian accounting automation platform built by accountants, for accountants. VERA is our AML/CTF client verification automation tool — purpose-built for accounting firms navigating Tranche 2 compliance. VERA handles VOI checks, AML screening, PEP checks, risk scoring, engagement letters, and record keeping automatically.

Visit nexautomate.com.au