For nearly two decades, AML/CTF compliance has been something other industries worried about — banks, casinos, remittance providers and financial institutions.

From 1 July 2026, that changes.

Australian accounting firms are now squarely within the regulatory perimeter. If your firm provides tax, bookkeeping, company formation, trust services, or other designated services, AML/CTF compliance for accounting firms is about to become a core operational obligation.

This guide explains what AML/CTF means, why it now matters, and how NeX Automate helps practices prepare with practical accounting automation, Client Verification Automation, and wider AI automation for accounting firms.

Try VERA Free — No Card Needed

Sign up and get 50 free credits to run live Client Verification checks and see how VERA handles VOI, screening and risk scoring for your firm.

Start Free – Get 50 Credits →What Does AML/CTF Actually Stand For?

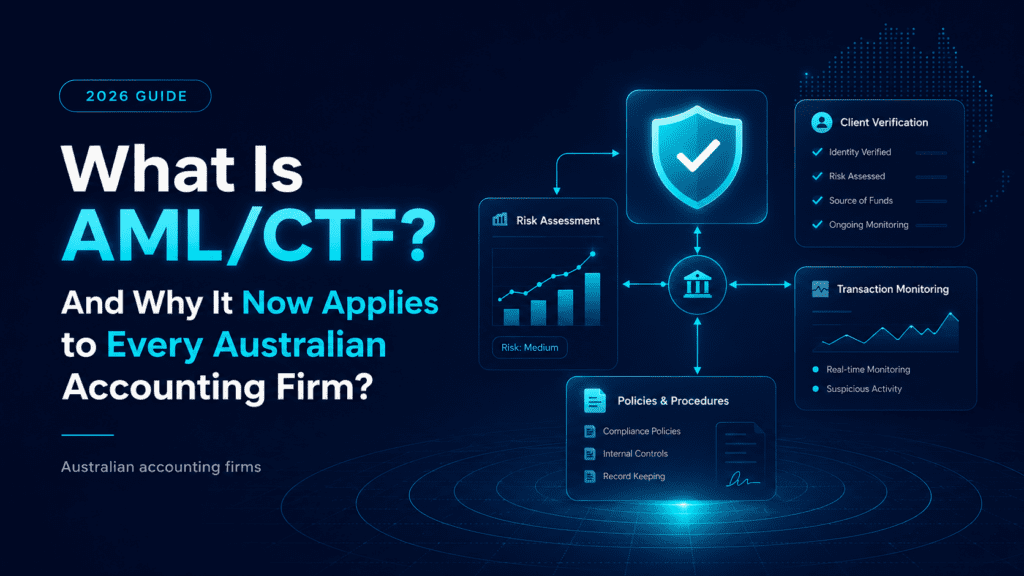

AML/CTF stands for Anti-Money Laundering and Counter-Terrorism Financing. It is a regulatory framework designed to detect, deter, and disrupt the movement of illegal funds through the legitimate economy.

In Australia, AML/CTF is governed by the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 and administered by AUSTRAC — the Australian Transaction Reports and Analysis Centre.

At its core, AML/CTF compliance requires regulated businesses to:

- Know who their clients are

- Understand the nature of the services they provide

- Assess client and transaction risk

- Monitor for unusual activity

- Report suspicious matters to AUSTRAC

- Keep proper records for audit and regulatory review

For accounting practices, this means AML/CTF compliance is not just a policy document. It becomes part of client onboarding, verification, record-keeping, staff training, and ongoing monitoring.

According to estimates cited by AUSTRAC and the Australian Criminal Intelligence Commission, billions of dollars are laundered through Australia each year. This is why stronger controls, better documentation, and reliable AML/CTF compliance software are becoming important for professional service firms.

Why Money Laundering Matters — The Scale of the Problem

Money laundering is not a victimless paperwork problem.

According to the Financial Action Task Force, between 2% and 5% of global GDP is laundered annually, equivalent to roughly US$800 billion to US$2 trillion. In Australia, serious and organised crime costs the economy up to $60.1 billion per year, according to the Australian Criminal Intelligence Commission.

Professional service providers, including accountants, bookkeepers, lawyers, conveyancers and company service providers, can be used as gatekeepers in laundering schemes — sometimes knowingly, but often without realising the risk.

That is precisely why the Attorney-General’s Department has extended the AML/CTF regime to capture professions that may be exposed to this risk. Your team must be able to identify clients properly, understand risk, document decisions, and prove that the right checks were completed.

This is where accounting automation for firms can make a major difference. Manual spreadsheets, scattered emails, ID attachments, and inconsistent notes are risky. A structured AML/CTF compliance software process helps firms keep client verification and compliance evidence organised.

What Are the Tranche 2 Reforms?

The original 2006 legislation captured “Tranche 1” entities such as banks, financial institutions, casinos, and remittance dealers. The Tranche 2 reforms extend the regime to “designated non-financial businesses and professions” known as DNFBPs.

These include:

- Accountants and bookkeepers providing designated services

- Lawyers and conveyancers

- Real estate agents

- Trust and company service providers

- Dealers in precious metals and stones

Australia was one of the last major economies in the FATF network to regulate these professions. Tranche 2 brings the country into line with international standards.

For accountants, the practical impact is clear: AML/CTF compliance will require stronger systems, clearer workflows, and better evidence management. Many practices are now looking at accounting automation, Client Verification Automation, and AI automation for accounting firms because manual compliance will become harder to manage at scale.

What Accounting Firms Must Do From 1 July 2026

From 1 July 2026, accounting firms that provide designated services will need to meet new AML/CTF obligations. These may include:

- Enrolling and registering with AUSTRAC as a reporting entity

- Developing a written AML/CTF Program covering risk assessment and internal controls

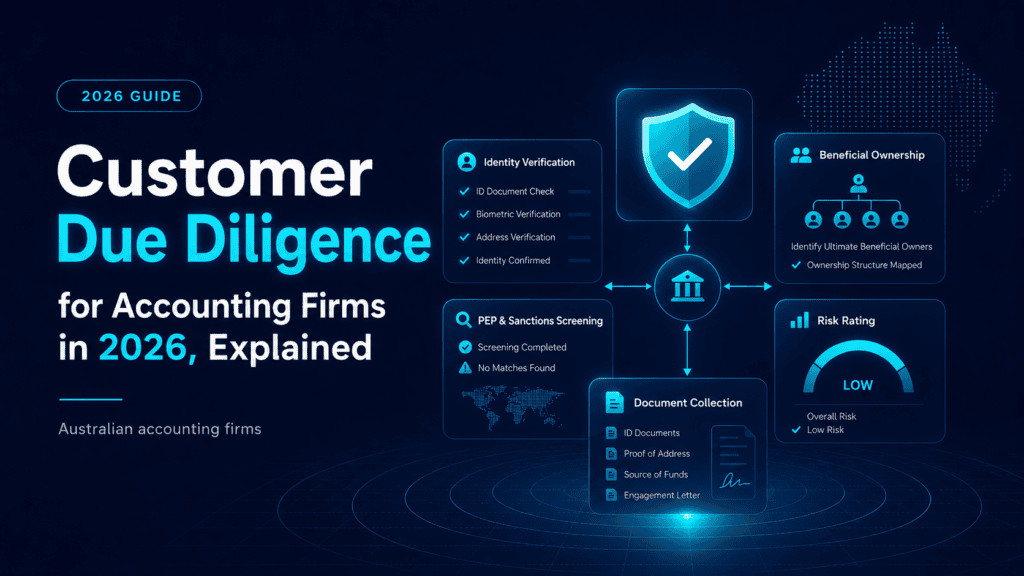

- Conducting Customer Due Diligence on new clients

- Verifying client identity and assessing risk

- Monitoring client relationships on an ongoing basis

- Reporting suspicious matters to AUSTRAC within strict timeframes

- Keeping records for a minimum of 7 years

- Training staff on their AML/CTF obligations

The biggest operational challenge will be consistency. One staff member may collect ID documents by email. Another may save notes in a spreadsheet. Another may forget to document a risk decision. Over time, these small gaps can create compliance exposure.

This is why AML/CTF compliance software and accounting automation for firms are becoming essential. They help standardise the process so every client goes through the same verification, screening, risk scoring, and record-keeping steps.

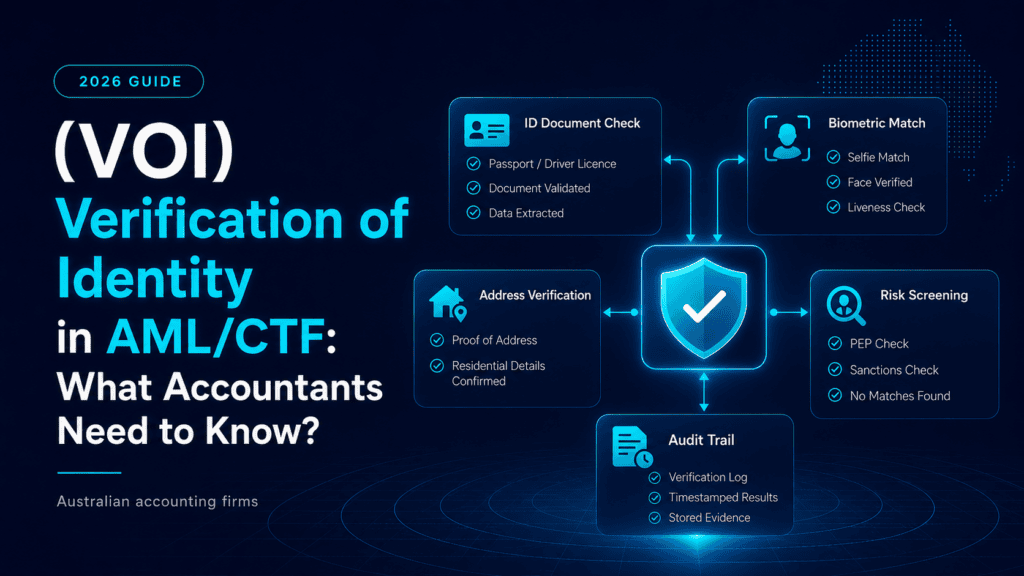

🤖 Meet VERA — Client Verification Automation

The single most time-consuming AML/CTF obligation is Customer Due Diligence — verifying identity, screening against watch lists, scoring risk, and documenting everything for audit. Done manually, this can take 15 to 30 minutes per client.

VERA automates this workflow end-to-end: automated VOI checks, AML/CTF watch-list screening, risk scoring, and audit-ready records — without unnecessary manual intervention.

Get AML Policies & Staff Training Sorted in 15 Minutes

Not sure how your team will get ready? Complete this quick intake form and we’ll prepare a draft AML/CTF policy for your firm — with your firm details, services, responsible people and onboarding process inserted.

Get My Draft AML Policy →Why Accounting Automation for AML/CTF Matters

AML/CTF compliance is not only about having a policy. It is about proving that your firm followed the right process every time. That means firms need systems that can:

- Collect client information securely

- Verify identity documents

- Screen clients against risk lists

- Record risk scores

- Store evidence for audit

- Trigger reminders and follow-ups

- Keep the compliance process consistent

Alongside VERA for Client Verification Automation, firms can also explore:

- Workpaper Automation for structured workpaper preparation

- ATO Automation for handling ATO-related document workflows

- ASIC Review Automation for simplifying ASIC annual review processes

Together, these tools show how AI automation for accounting firms can support compliance, client service, and internal productivity.

AML & VOI Checks for Less Than a Coffee

VERA is designed to reduce the manual workload involved in client verification and AML/CTF preparation. It helps firms by:

- Automating client identity checks

- Supporting VOI workflows

- Screening clients against AML/CTF risk lists

- Applying structured risk scoring

- Keeping audit-ready records

- Reducing staff time spent chasing documents

- Creating a more consistent onboarding experience

At just $25 per hour of bot runtime, VERA gives firms a cost-effective way to manage a major compliance workload — paying only when the automation is actually working.

P.S. One thing most compliance articles don’t tell you: the legislative deadline is not the only deadline. Implementing a verification process takes time. The firms that will be most comfortably compliant on 1 July are the ones that start their setup early and give themselves room to configure everything properly.

Key Takeaways

- AML/CTF compliance becomes mandatory for Australian accounting firms from 1 July 2026.

- It covers client verification, risk assessment, reporting, record-keeping, and ongoing monitoring.

- The regime is administered by AUSTRAC under the AML/CTF Act 2006 and expanded by Tranche 2 reforms.

- Firms must register, build a program, conduct CDD, monitor, report, and keep records for 7 years.

- VERA from NeX Automate supports the most time-consuming obligation: client verification.

- Accounting automation supports wider firm efficiency across AML/CTF, ATO, ASIC, and workpaper workflows.

🤖 Automate AML/CTF Compliance with VERA

Reduce manual verification work. Keep audit-ready records. Start your Client Verification Automation today — your first 50 credits are on us.

Start Free – Get 50 Credits →Still comparing your options? See our breakdown of the best AML/CTF compliance software for accounting firms to find the right fit for your practice.